The 1.3 Trillion-Dollar Catalyst: How the OpenAI, Anthropic, and grok IPOs will Supercharge the Nuclear Renaissance

Data center and AI scaling has fundamentally broken the existing power grid

The impending IPOs grok, OpenAI and Anthropic are effectively massive capital-raising exercises designed to fund the physical infrastructure of artificial intelligence. When those billions of dollars are deployed, they will act as a powerful catalyst for the nuclear energy and uranium sectors, transforming long-term energy forecasts into immediate corporate mandates.

The capital mobilized by the tech sector for data centers in 2025 and 2026 alone exceeds the inflation-adjusted cost of the Manhattan Project, the Marshall Plan, and the Apollo Program combined.

These hyperscalers are building multi-gigawatt data center clusters that require firm, dispatchable, 24/7 power. Only the dreamers think Wind or solar can meet this density leaving nuclear power as the only viable zero-carbon solution. Microsoft alone recently disclosed an $80 billion backlog of Azure orders that cannot be fulfilled simply due to a lack of power. The $650 Billion Bottleneck: Big Tech Is Spending a Fortune on AI — But They Can’t Plug It In

Macro Notes covers this well highlighting the ‘Transformer’ choke point!

Historically, the uranium market was dictated by over regulated public utilities moving at a bureaucratic Snails pace.

The new players with functionally unlimited capital who are desperate for power may be about to shake the tree in the nuclear sector especially for those who haven’t being paying attention.

For a very short term history lesson try:

Microsoft underwrote the restart of Three Mile Island,

Amazon backing advanced reactor developer X-energy, and

Google has partnered with Kairos Power.

China’s amazing nuclear power build rate. Nearly every Chinese nuclear project that has entered service since 2010 has achieved construction in 7 years or less.

India has its groove on in the nuclear power race and securing the fuel to do it

France is getting its Nuclear Power mojo back and doubling down

All of this will bid up the price of available U308 and nuclear fuel capacity, pulling the long-term price floor for uranium significantly higher.

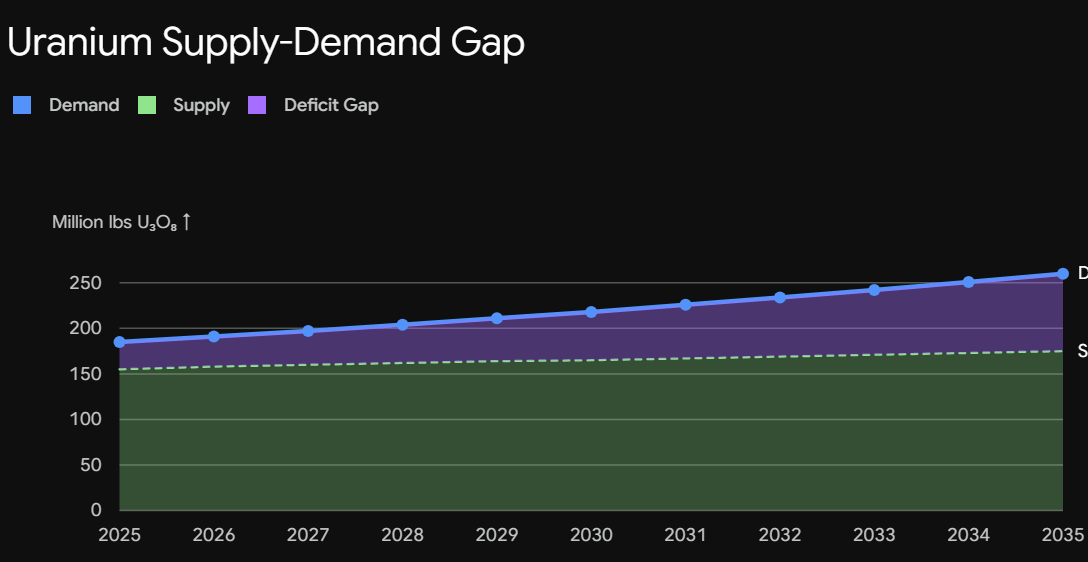

Pouring Fuel on the U308 and Nuclear Fuel Structural Deficit

This is all colliding head-on with a uranium market already defined by a severe structural supply deficit and underinvestment in both the reactors required and exploration. Global reactor requirements have consistently outpace primary mine supply, and the secondary inventory buffers that historically plugged this gap are largely depleted from the Uranium Markets as stated by The Nuclear industry body UXC. while full access to UxC’s information is provided only to paying subscribers. It recently warned of the supply crunch.

On top of the Huge IPOs, the money Data centres world wide to date and to be add for 2026-2027 is itself a catalyst to the current $150+ market referecence contract prices. The 14 largest publicly traded data center operators spent roughly $450 billion globally last year.

Projections for the next 24 months reflect a near-doubling of investment, driven almost entirely by the race to build out AI training and inference capacity. This is expected to approach $750 billion. The EU 20 billion plan includes power “In just a few months we have set up a record of 12 AI factories. And we are investing EUR 10 billion in them. This is not a promise – it is happening right now, and it is the largest public investment for AI in the world, which will unlock over ten times more private investment. Our goal is that every company, not only the big players, can access the computing power it needs. We want AI developers to compete based on how innovative they are, not just on their access to chips or the size of their financial firepower.”

A few years ago the Eu’s $20 billion may have seemed a huge amount.

The race for power will occur with this trillion dollar money flow being shortly convert into countries, power utilities and hyperscaler contracts need for the secure 24/7 power required for all industrial and domestic power users not just physical data center build-outs. Counties and companies are competing in this race!

Short term Breathing space for some

U.S. Department of Energy Surplus Plutonium Disposition Program. The plutonium will act as a bridge fuel until SMR developers can begin to produce High-Assay Low-Enriched Uranium, or HALEU fuel. Clearly the bottleneck extends well beyond the extraction of yellowcake. Silex Systems and Global Laser Enrichment (GLE), transitions from an R&D priority to an absolute geopolitical and commercial necessity to keep these new AI clusters fueled.

Global Laser Enrichment’s Paducah Project is more than a "Virtual Mine" It is turning nuclear waste dump into one of the largest "virtual uranium mines" on the planet. GLE is pushing aggressively toward full commercial deployment, targeting operations around 2030. SILEX Global Laser Enrichment isn’t just about natural-grade uranium. Laser enrichment is arguably the most viable Western path to producing High-Assay Low-Enriched Uranium (HALEU)—the specialized fuel enriched between 5% and 20% that is strictly required for the next generation of Small Modular Reactors (SMRs). The Paducah Project output of UF6 skipd the cost of traditional U308 mines.

The Medium term

The 5-Year Outlook: Looking at the 2025–2030 window, total capital investment across the data center value chain (real estate, power infrastructure, and IT hardware like servers and GPUs) is projected to reach between $3 trillion and $7 trillion. Last year for those with short memories McKinsey estimates that roughly $1.3 trillion is earmarked specifically for the “energizers”—investments in power generation, transmission, cooling, and electrical equipment.

UXC 5-Year Outlook for uranium has moved from very optimistic to a bit more realistic. Noting they have never really got it right!

This is not a one shot wonder - The defining characteristic of the next five years is the inability of the supply side to quickly respond to price signals, reinforcing the structural deficit.

Ultimately, these tech IPOs will fund a wave of energy procurement that the current uranium supply chain is entirely unequipped to absorb, forcing a dramatic repricing across the entire nuclear fuel cycle. The race is not just between them!

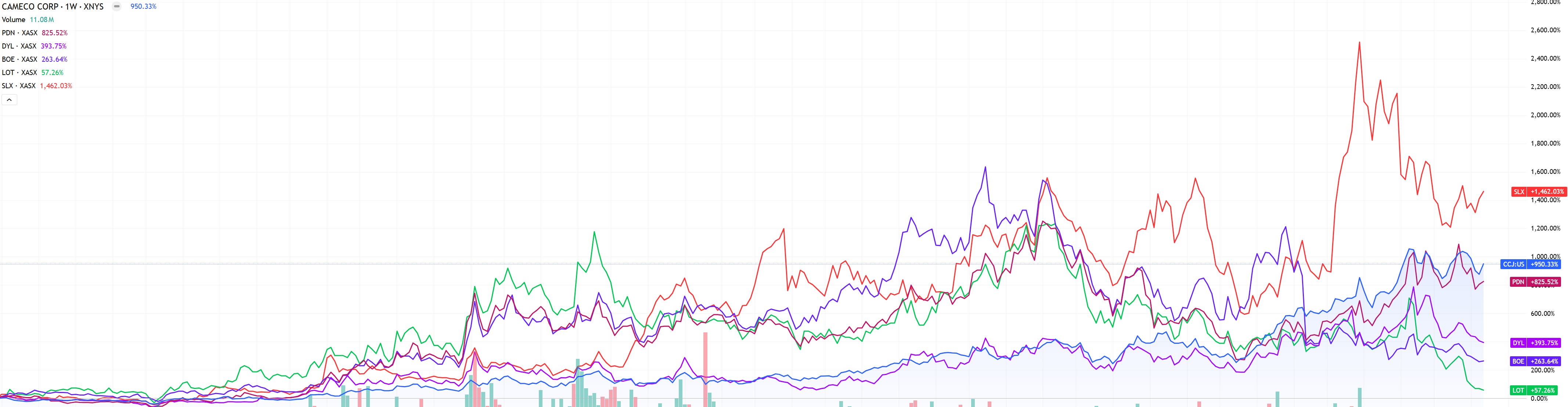

The five year review in Oz (In $AUD except for Cameco)

Waiting sucks eggs. Missing the start might be worse of course. Has The race for power moved to the Australian u308 miners and Silex?

Cameco is not on the ASX It is my personal base line in the sector moving from the USD$20 range in mid-2021 to over USD$110+ by mid-2026 (About $27.81642AUD to $152.99031AUD)

While this has been fantastic. This black ducks thinks Paladin was one of the premier ASX "restart plays" of this cycle. A few years ago it was trading for a few cents. Over the last five years, as it successfully funded, refurbished, and restarted operations, its stock price skyrocketed by over 1,000% for me. I smile a lot at this survival story despite the several capital raisings required that many grumbled about while I put my hand in my pocket and brought more.

Lotus has had high volatility and huge swings. Its sub 10cents price in 2019 was not my entry point! 0.625 close on Friday 29 May 2026 is not close to this year’s high above $3!

Boss Energy has almost tripled from five years ago. Not close to the highs of above $6 in Jan 2024! Close on Friday 29 May 2026 $1.270

NextGen Energy is on fire despite the management funding a Formular one team!

DEEP YELLOW John Borshoff leaving was a bit of a shock! It was above $2.83 When that announcement dropped back in October 2025 , that sharp haircut instantly repricing the “Borshoff premium.” Close on Friday 29 May 2026 $1.605

NB -I have excluded BHP, Torro and a few other Aussie in the secotor.

When John Borshoff the industry's most proven mine-builder exits stage left before the heavy earth-moving begins, it allows is a look at sector-wide execution and U308 mining risks. Cameco McArthur River and Key Lake sites impact by the Smooth Stone River bridge collapse has been fixed now. Issues for Boss and at Paladin and Lotus mines including PDN- Unseasonal, intense rainfall and flooding in early 2025 severely disrupted operations. Boss suffered a massive 42% share price crash when they reported that their uranium recovery rates were lower than expected. The chemistry simply wasn’t behaving exactly as the models predicted. Lotus had the triple whammy Lotus has had the messiest 2026.

Kayelekera in Malawi requires a massive amount of sulphuric acid to process its ore- Exposed severe logistical fragility.

The Data Shock: In early 2026, while replacing instrumentation in the leach circuit, Lotus discovered discrepancies in their previously reported mined grade and recovery data. They had to formally retract the figures, which absolutely crushed investor confidence and sent the stock tumbling 30% to sub-$1.00 levels in early 2026.

The Fire: Just to add insult to injury, in April 2026, a fire broke out in the drying and packaging area of the mine, suspending processing operations for roughly three weeks before resuming later in the month.

The Aussie 2026 Status:

Lotus -They are mining plenty of ore, finishing an on-site acid plant rebuild in mid-2026 to fix the supply chain vulnerability. The market currently has LOTUS firmly in the Dog box. Lotus is entering June 2026 in the middle of an active corporate intervention to fix the Kayelekera processing bottlenecks.

Paladin is heading into June looking bulletproof, having completely shaken off the operational hangover of 2025.

Boss Energy’s shift to a wider-spaced wellfield design for the technical fix for Honeymoon's chemistry issues. They are confidently forecasting annual production of around 2 million pounds of U3O8, putting them right on the doorstep of their 2.45Mlb nameplate capacity.

Paladin and Boss survived the "restart valley of death" and are now or about to printing cash in the high-price Long term contract environment. Lotus proved that without ruthless technical execution, possessing a massive uranium resource doesn't automatically equal cash flow. They may be the biggest turnaround story IF they deliver as expected now!

Has the current or upcoming ‘Race for power’ shifted to the Australian U308 miners and Silex yet?

I think not!

This is not a masterclass in how the market prices risk between uranium developers and active producers. It’s clearly not investment advice either.

Pounds in the ground are worth a fraction of pounds in the drum. Until a developer actually makes an F.I.D., crosses the Rubicon of start up and starts successfully extracting u308, the market will apply a heavy risk discount, no matter how good the resource estimate looks.

Personally, watching China build is my favorite past time while I wait.

“Demand from anywhere is demand from everywhere” from Mr Nick Lawson and Mr Ben Finegold at Ocean Wall may have said this.

“Demand from anywhere is demand from everywhere”

The China Factor: When China announces the construction of 10 new reactors per year, they aren’t just tightening the u308 market. They are directly competing for the exact same finite pool of physical uranium that Japanese, US and European utilities have yet to secure.

It’s a Global Squeeze: Because the supply pool is global any and all demand immediately tightens the market and will raises the price floor for everywhere and everyone.

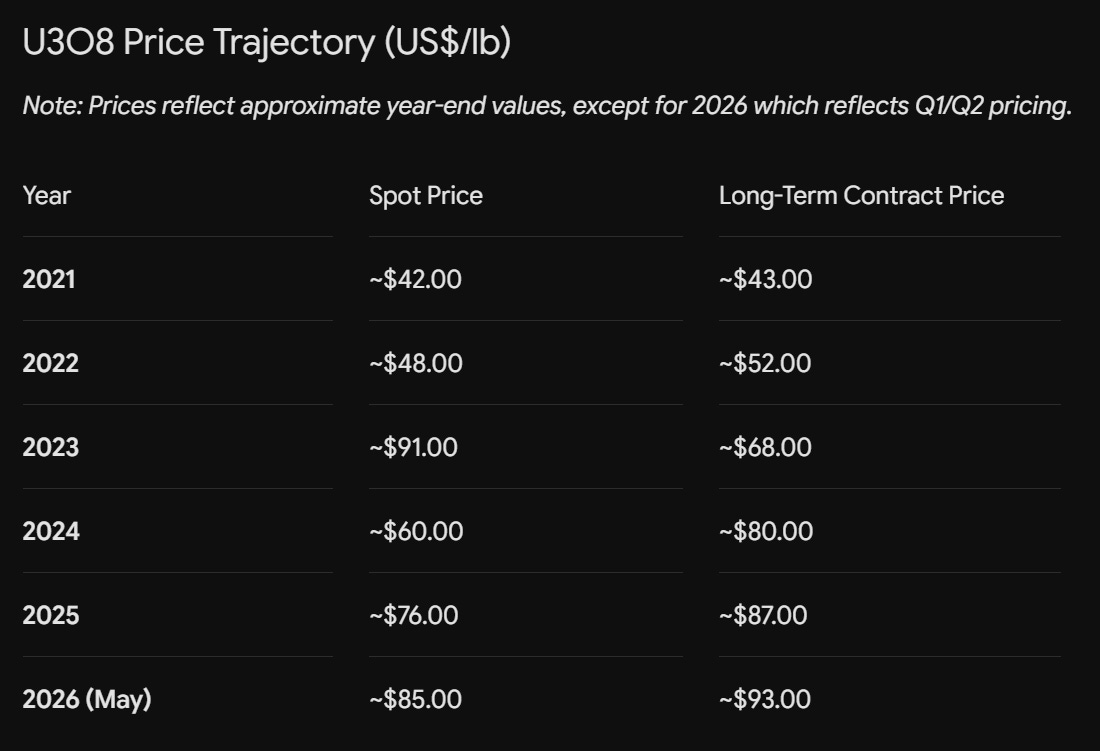

The Five year Price time frame for u308 from Cameco looks ok.

What’s more interesting is news from Tim Gitzel, the President and CEO of Cameco following the company’s Q1 2026 results and recent industry conferences, Gitzel has characterized the current landscape as the

“best environment for nuclear in four decades.”

roughly 70% of the uranium supply required by global reactors for the next two decades (over 3 billion pounds) remains uncontracted. As utilities scramble to lock in supply, this is aggressively driving up long-term contract prices, regardless of what the spot market is doing on any given day.

pointed out a fundamental truth of the nuclear fuel cycle: price elasticity doesn't exist for utilities.

He mentions ceiling prices of over USD $150 in some current long-term market referenced contracts!

On AI and datacentres- "It's a demand increase like we haven't seen, and I don't think we've seen the end of it yet."

I agree with Mr Gitzel on almost everything except ‘I think the AI datacentre ‘demand increase’ is yet to begin.’

It is from a RACE China’s secret weapon in AI race with US? Lots of cheap energy

“BloombergNEF, a research provider, estimates that China will add more than six times as much electricity generation capacity as the US over the next five years.”

“A typical data centre can consume as much electricity as 100,000 households, while next-generation “hyperscale” facilities can gobble up as much power as two million homes, according to the International Energy Agency (IEA).”

The race is on at so many levels.

The Significant Price rises coming to Long Term contracts required for this are just lining up at the starting blocks.

June news other than my waffle out soon while we are waiting for what’s coming.

Domestic Uranium Production Report - 2025 Next Release Date June 2026